|

| "I warn you, Sir! The discourtesy of this bank is beyond all limits. One word more and I — I withdraw my overdraft!" ---- Cartoon from Punch Magazine Vol. 152, June 27, 1917 |

An overdraft occurs when money is withdrawn from a bank account and the available balance goes below zero. In this situation the account is said to be "overdrawn". If there is a prior agreement with the account provider for an overdraft, and the amount overdrawn is within the authorized overdraft limit, then interest is normally charged at the agreed rate. If the negative balance exceeds the agreed terms, then additional fees may be charged and higher interest rates may apply.

Reasons for overdrafts

Overdrafts occur for a variety of reasons. These may include:- Intentional short-term loan - The account holder finds themselves short of money and knowingly makes an insufficient-funds debit. They accept the associated fees and cover the overdraft with their next deposit.

- Failure to maintain an accurate account register - The account holder doesn't accurately account for activity on their account and overspends through negligence.

- ATM overdraft - Banks or ATMs may allow cash withdrawals despite insufficient availability of funds. The account holder may or may not be aware of this fact at the time of the withdrawal. If the ATM is unable to communicate with the cardholder's bank, it may automatically authorize a withdrawal based on limits preset by the authorizing network.

- Temporary Deposit Hold - A deposit made to the account can be placed on hold by the bank. This may be due to Regulation CC (which governs the placement of holds on deposited checks) or due to individual bank policies. The funds may not be immediately available and lead to overdraft fees.

- Unexpected electronic withdrawals - At some point in the past the account holder may have authorized electronic withdrawals by a business. This could occur in good faith of both parties if the electronic withdrawal in question is made legally possible by terms of the contract, such as the initiation of a recurring service following a free trial period. The debit could also have been made as a result of a wage garnishment, an offset claim for a taxing agency or a credit account or overdraft with another account with the same bank, or a direct-deposit chargeback in order to recover an overpayment.

- Merchant error - A merchant may improperly debit a customer's account due to human error. For example, a customer may authorize a $5.00 purchase which may post to the account for $500.00. The customer has the option to recover these funds through chargeback to the merchant.

- Chargeback to merchant - A merchant account could receive a chargeback because of making an improper credit or debit card charge to a customer or a customer making an unauthorized credit or debit card charge to someone else's account in order to "pay" for goods or services from the merchant. It is possible for the chargeback and associated fee to cause an overdraft or leave insufficient funds to cover a subsequent withdrawal or debit from the merchant's account that received the chargeback.

- Authorization holds - When a customer makes a purchase using their debit card without using their PIN, the transaction is treated as a credit transaction. The funds are placed on hold in the customer's account reducing the customer's available balance. However the merchant doesn't receive the funds until they process the transaction batch for the period during which the customer's purchase was made. Banks do not hold these funds indefinitely, and so the bank may release the hold before the merchant collects the funds thus making these funds available again. If the customer spends these funds, then barring an interim deposit the account will overdraw when the merchant collects for the original purchase.

- Bank fees - The bank charges a fee unexpected to the account holder, creating a negative balance or leaving insufficient funds for a subsequent debit from the same account.[1]

- Playing the float - The account holder makes a debit while insufficient funds are present in the account believing they will be able to deposit sufficient funds before the debit clears. While many cases of playing the float are done with honest intentions, the time involved in checks clearing and the difference in the processing of debits and credits are exploited by those committing check kiting.

- Returned check deposit - The account holder deposits a check or money order and the deposited item is returned due to non-sufficient funds, a closed account, or being discovered to be counterfeit, stolen, altered, or forged. As a result of the check chargeback and associated fee, an overdraft results or a subsequent debit which was reliant on such funds causes one. This could be due to a deposited item that is known to be bad, or the customer could be a victim of a bad check or a counterfeit check scam. If the resulting overdraft is too large or cannot be covered in a short period of time, the bank could sue or even press criminal charges.

- Intentional Fraud - An ATM deposit with misrepresented funds is made or a check or money order known to be bad is deposited (see above) by the account holder, and enough money is debited before the fraud is discovered to result in an overdraft once the chargeback is made. The fraud could be perpetrated against one's own account, another person's account, or an account set up in another person's name by an identity thief.

- Bank Error - A check debit may post for an improper amount due to human or computer error, so an amount much larger than the maker intended may be removed from the account. Same bank errors can work to the account holder's detriment, but others could work to their benefit.

- Victimization - The account may have been a target of identity theft. This could occur as the result of demand-draft, ATM-card, or debit-card fraud, skimming, check forgery, an "account takeover," or phishing. The criminal act could cause an overdraft or cause a subsequent debit to cause one. The money or checks from an ATM deposit could also have been stolen or the envelope lost or stolen, in which case the victim is often denied a remedy.

- Intraday overdraft - A debit occurs in the customer’s account resulting in an overdraft which is then covered by a credit that posts to the account during the same business day. Whether this actually results in overdraft fees depends on the deposit-account holder agreement of the particular bank.

Trimming Monthly Expenses Can Lead to Big Savings

Sometimes it's the little things that add up. Stopping the small spending leaks in your life may amount to significant savings over time.

One of the most stress inducing factors in any household involves the struggle that debt and bills bring to one's life. The stress from being in debt can cause severe physical and mental ailments, tear down a marriage, and impact a credit score to the point where even obtaining a loan for a used car will become difficult at best. While there are many ways to get out of debt, one of the best methods involves simply saving money. While it may sound easier said than done, these three simple steps will have you on the pathway to saving money and getting out of debt quickly.

When you hear the word “budget”, what does it mean do you? If you’re like most people, you probably think of it as an unpleasant activity that means you have to financially deprive yourself. This couldn’t be further from the truth, yet this is the typical reason that most budgets fail.

|

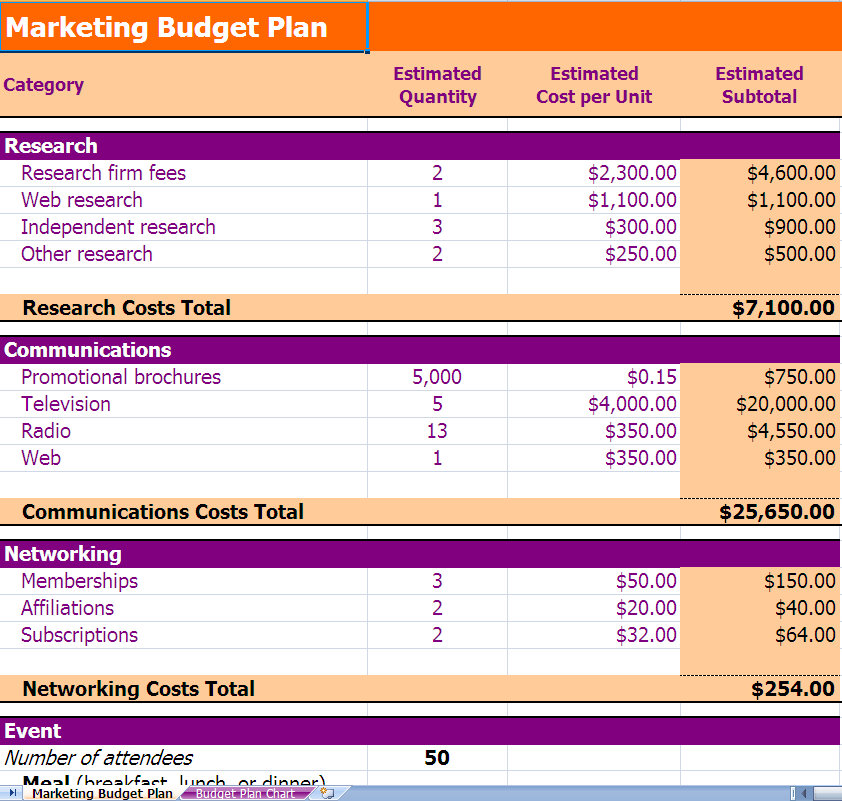

Download Budget plan excel workbook |

Creating a budget may not sound like the most exciting thing in the world to do, but it is vital in keeping your financial house in order. Before you begin to create your budget it is important to realize that in order to be successful you have to provide as much detailed information as possible. Ultimately, the end result will be able to show where your money is coming from, how much is there and where it is all going.